16 years

Arizona credit repair since 2010

State 48 Credit is Arizona's hard inquiry removal service - and we dispute and remove every unauthorized hard inquiry from Experian, Equifax, and TransUnion for a flat one-time fee with a 100% money-back guarantee. Every unauthorized inquiry on your credit report is lowering your score - sometimes by as much as 5 to 10 points per pull, and far more when multiple inquiries stack.

If someone pulled your credit without your permission, if you see inquiries you do not recognize on any bureau, or if you simply have too many hard inquiries dragging your score down, we remove them. Serving Phoenix and all of Arizona.

No payment until after your free consultation. Zero pressure. We review your report first and tell you exactly which inquiries can be removed before you spend anything.

Founder

Robert Garcia

Hard Inquiry Removal Specialist | Serving Phoenix and all of Arizona

Robert personally reviews your report, identifies which pulls are actually unauthorized, and gives you a straight answer before you spend a dollar.

16 years

Arizona credit repair since 2010

15,892 items deleted

Including thousands of hard inquiries

4.9 star Google rating

412 verified Arizona reviews

All 3 bureaus

Experian, Equifax, and TransUnion

Hard inquiries can only be removed before their 24-month expiration if they were unauthorized - placed without your permission or without a valid FCRA permissible purpose. To remove them, you submit a written dispute to Experian, Equifax, or TransUnion citing FCRA Section 604 and requesting deletion. State 48 Credit handles the full process - inquiry audit, custom dispute letters, bureau submission, and follow-up - for a flat one-time fee with a 100% money-back guarantee.

A hard inquiry is a record placed on your credit report when a lender, creditor, landlord, or another entity pulls your credit to evaluate you for a financial product. Hard inquiries usually lower your score by 5 to 10 points each and remain visible on your report for two full years, even though their scoring impact usually fades after about 12 months.

A hard inquiry happens when you apply for credit, such as a mortgage, auto loan, credit card, apartment, or personal loan. A soft inquiry happens when your credit is checked for a non-lending purpose like a background check, pre-approval, or your own monitoring. Soft inquiries do not affect your score and lenders do not see them.

Checking your own credit never hurts your score. The distinction that matters is this: only hard inquiries affect score calculations, and only unauthorized hard inquiries can be disputed and removed early. Learn how our Arizona credit repair process works.

A single hard inquiry usually lowers your score by 5 to 10 points, but the real damage comes from stacking. Multiple recent pulls suggest active credit-seeking behavior to lenders, which can make approvals harder even when the rest of the file is workable. Hard inquiries stay on your report for 24 months and typically stop affecting score calculations after 12 months.

1 to 2 inquiries

Usually around 5 to 15 points total.

3 to 5 inquiries

Often 15 to 30 points with noticeable approval friction.

6 or more inquiries

Commonly 30 to 50+ points and a major red flag in underwriting.

Yes. The score improvement happens on the date the inquiry is removed because scoring models recalculate with each change to your file. A client who gets eight unauthorized pulls removed in one round sees the benefit of all eight removals at the same time. That is why professional hard inquiry removal can create some of the fastest score movement we generate.

In Arizona, especially in Phoenix, Tucson, and border-connected communities like Yuma, dealership multi-pulls and identity-theft inquiry trails are among the most common patterns we see. Clients often do not realize how much of their score drop is tied to inquiries until we map the full report and show them where the damage is stacking.

The strongest hard-inquiry dispute ground is also the one most people miss: somebody pulled your credit without your explicit permission. Under the Fair Credit Reporting Act, anyone pulling your report must have a permissible purpose. If they did not, the inquiry is removable.

The most common unauthorized situations we see are dealership shotgunning, identity theft applications, lenders you have never heard of appearing on your report, and employers or landlords generating a hard pull where a soft inquiry should have been used instead. If fraud is involved, an FTC identity theft report strengthens the dispute even more. See how we handle identity-theft recovery in Arizona.

You hand over your driver's license for what feels like one credit check and later discover four, five, or six inquiries from different lenders. You may have authorized one application, but not every extra pull that followed. Every inquiry beyond what you explicitly approved deserves a closer legal review.

Rate shopping is the exception most consumers hear about but almost nobody explains correctly. FICO allows multiple pulls for the same mortgage or auto-loan shopping window to be treated as one inquiry for scoring. That does not mean every inquiry in a cluster is automatically harmless or authorized.

Multiple mortgage pulls inside the 14-to-45-day FICO rate-shopping window are usually treated as a single inquiry for scoring purposes.

Auto-loan shopping follows the same basic window. A dealer can shop rates, but unauthorized extra pulls beyond what you approved are still disputable.

Credit cards, personal loans, and other revolving-credit applications do not qualify for rate-shopping treatment. Five applications means five separate inquiries.

The problem begins when a dealership spreads pulls across different days, different lenders, or different application amounts. That breaks the clean rate-shopping picture and can leave you with multiple real scoring hits. We review every inquiry in the cluster and dispute the ones that go beyond what you actually approved.

Hard inquiries are reported separately by each bureau. Removing an inquiry from one report does not remove it from the others. That is why we handle bureau disputes as a coordinated process, not three disconnected tasks.

Experian is the bureau most commonly affected by identity-theft inquiry trails and dealership multi-pull situations. Their dispute process often turns on the exact documentation used to prove the pull lacked your permission or a valid permissible purpose.

Experian also encourages portal-based disputes, but template submissions through that system are among the most frequently rejected. Custom written disputes with the specific FCRA basis spelled out consistently give Arizona clients a stronger paper trail and a stronger removal record.

Equifax inquiry disputes are won or lost on documentation. The bureau needs a precise challenge to the permissible purpose behind the inquiry, especially when the lender claims there was a valid application.

When fraud is involved, Equifax often requires a tighter identity-theft documentation package than consumers expect. We track the investigation window, the creditor response, and the follow-up round so the dispute does not stall out after the first reply.

TransUnion inquiry disputes frequently benefit from being paired with identity-theft documentation, especially when the inquiry trail touches multiple lenders. We handle the initial dispute, the creditor-verification challenge, and the follow-up process if the first result is a form response.

Addressing TransUnion correctly matters because a dispute sent to the wrong contact channel can cost time inside the 30-to-45-day FCRA window. We submit the dispute record the right way from the start so the paper trail stays clean.

If the same unauthorized pull appears on two or all three bureaus, it has to be disputed on every bureau where it appears. Removing it from one report does not automatically clear the others.

For Arizona residents, the process is fully remote. Whether you are in Phoenix, Tucson, Yuma, or anywhere else in the state, we run the same multi-bureau process without requiring an office visit.

This is the exact process we use when a client hires us for inquiry removal. The goal is to identify what was unauthorized, dispute it correctly, and keep pressure on the bureau until the inquiry is either deleted or properly explained.

We review your three-bureau report, identify every hard inquiry, and determine which pulls were unauthorized or outside what you actually approved.

Every inquiry gets a bureau-specific legal argument built around the facts of your case, not a template letter copied from the internet.

We dispute the inquiries directly with Experian, Equifax, and TransUnion on your behalf so you are not juggling three separate timelines.

If a bureau verifies an inquiry, we review the response, escalate when needed, and use follow-up documentation such as FTC identity theft reporting where the facts support it.

Once the inquiry comes off, we document the result and the score impact so you know exactly what changed on each bureau.

A proper hard inquiry removal letter has to do more than say "I dispute this inquiry." It needs the specific creditor name, inquiry date, and bureau, a clear statement that the pull was unauthorized, the exact permissible-purpose violation under FCRA Section 604, a demand for deletion, and supporting documentation when fraud or identity theft is involved.

Template letters fail because they usually stop after item one. Bureaus see thousands of generic inquiry disputes every week and know exactly how to answer them with a form denial. If you tried DIY first and hit a wall, that usually does not mean the inquiry was valid. It means the legal framework in the letter was too weak. See how our process differs from DIY.

Inquiry removal is available as a focused add-on or as part of the more comprehensive restoration packages. The free consultation shows you which option makes sense before you pay anything.

All unauthorized inquiries removed across all three bureaus.

Best for: Adding inquiry cleanup to an active repair package.

View OptionThree-bureau negative-item removal plus hard inquiry removal.

Best for: Collections, late payments, charge-offs, and inquiry damage together.

View OptionAll three bureaus, inquiry removal, ChexSystems, InnoVis, and full restoration support.

Best for: Identity theft, inquiry trails, ChexSystems, and multi-system cleanup.

View OptionServing Phoenix and all of Arizona - every inquiry-removal service is delivered remotely, with no office visit required.

Inquiry removal alone can produce meaningful score increases when multiple unauthorized pulls are cleared at once. When it is paired with broader dispute work, the total score jump can be dramatic.

Destiny came to us as an identity-theft victim with 17 fraudulent accounts, a collapsed score, and an inquiry trail spread across Experian, Equifax, and TransUnion. We removed the fraudulent accounts, cleared the unauthorized inquiry trail those applications created, and restored the systems that were blocking normal banking access.

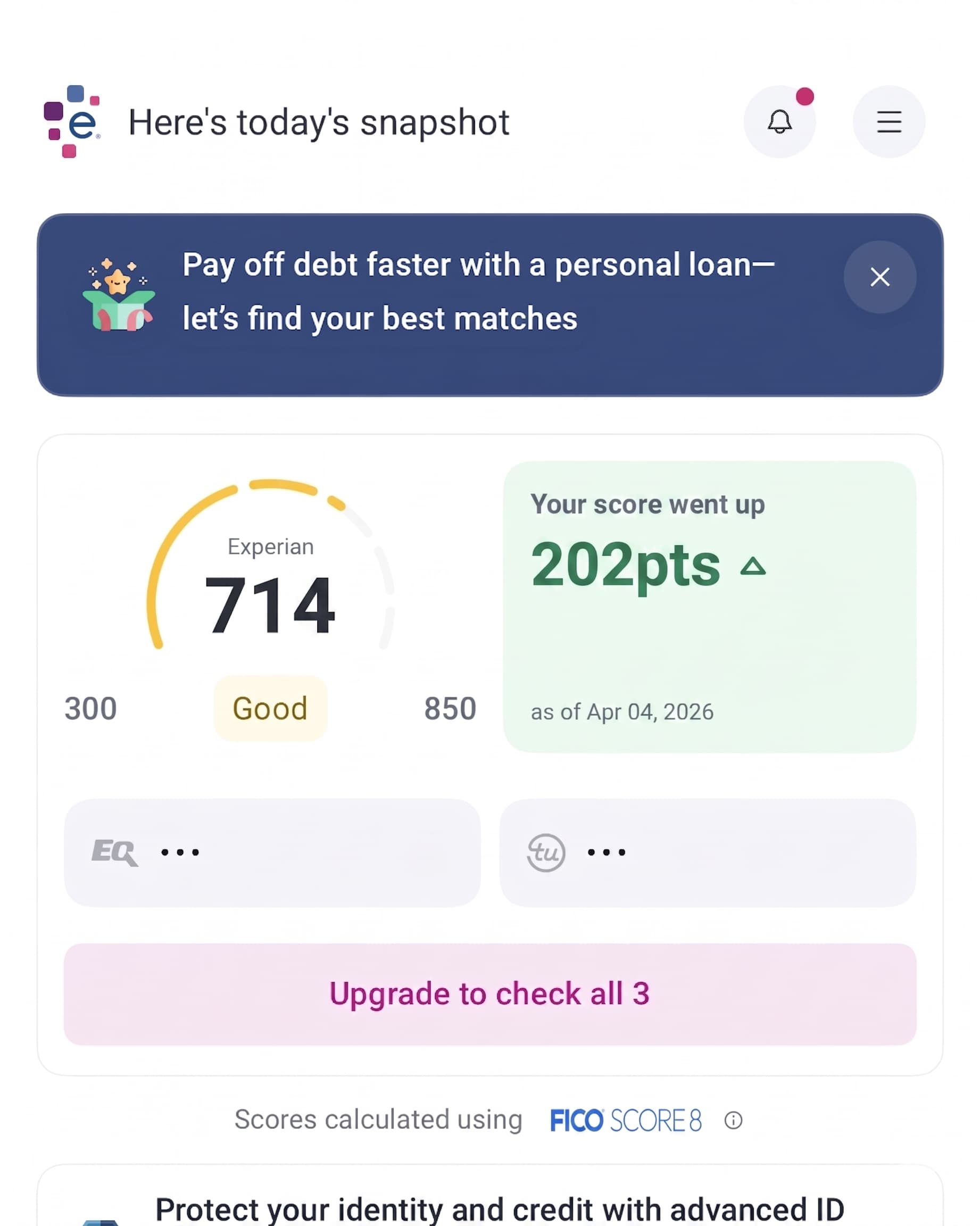

Final result: score increased from 512 to 714, ChexSystems was cleared, and the file was back in working order in 88 days. See full Arizona credit repair results.

"Someone stole my identity and completely destroyed my credit. I had 17 fraudulent accounts and didn't know where to start. Robert and his team removed all of them in under 90 days. I went from a 512 to a 714. I can actually do things again."

Destiny R. | Arizona Client | +202 points | Identity Theft Recovery

202-point increase

Fraudulent accounts and unauthorized inquiries removed across all three bureaus in 88 days.

"I tried disputing on my own for 8 solid months and kept hitting walls. State 48 removed 6 items in 38 days using dispute strategies I didn't even know existed. The custom approach is completely different from anything out there."

Priya N. | Chandler, AZ | +127 points | 38 days

"I had no idea how many inquiries were on my report or that most of them shouldn't have been there. State 48 removed them and several other items - my score jumped over 150 points. I qualified for my mortgage six weeks later."

Marcus D. | First-Time Home Buyer | Inquiries + Collections Removed

These are the exact questions Arizona clients ask when they discover hard inquiries on their report and want to know whether they are actually removable.

A hard inquiry is a record placed on your credit report when a lender or creditor pulls your credit to evaluate you for a financial product. Hard inquiries usually lower your score by about 5 to 10 points each, stay on your report for two years, and remain visible to lenders the full time. Soft inquiries from background checks, pre-approvals, or checking your own credit do not affect your score at all.

Hard inquiries can only be removed early when they were unauthorized, meaning they were placed without your permission or without a valid permissible purpose under the FCRA. The removal process requires a written dispute to Experian, Equifax, or TransUnion that identifies the inquiry, explains why it was unauthorized, and demands deletion. State 48 Credit handles the audit, custom dispute letters, bureau submission, and follow-up for a flat one-time fee.

No. If you genuinely authorized the credit pull by applying for a loan, credit card, apartment, or similar financial product, the inquiry cannot be removed before it falls off naturally after 24 months. The only inquiries that can be legally disputed and removed are the unauthorized ones.

Removing hard inquiries usually improves your score by about 5 to 10 points per inquiry removed, with the total impact depending on how many are removed and how damaged the file already is. Clients who remove several inquiries at once often see some of the fastest score jumps we produce in any category of dispute work.

Hard inquiries stay on your credit report for 24 months from the date they were placed. Their scoring impact usually fades after 12 months, but lenders can still see them for the full two-year period unless they are removed through a successful dispute.

An inquiry you do not recognize is either an unauthorized pull or a warning sign of identity theft. The first step is to identify the lender name, the date of the inquiry, and whether you have any memory of authorizing that entity to pull your credit. If you do not, it should be reviewed for dispute immediately.

Yes. Pulling your credit without your permission and without a valid permissible purpose is a Fair Credit Reporting Act violation. If no lawful purpose existed, the inquiry is removable and the entity that placed it may have exposed itself to legal liability.

You dispute a hard inquiry by sending a written challenge to the bureau identifying the inquiry, the creditor that placed it, the reason it was unauthorized, and the FCRA basis for deletion, usually Section 604 or Section 611. The bureau then has 30 to 45 days to investigate and respond. Template letters usually fail because they do not make the legal basis specific enough.

Yes, but auto-loan rate shopping is treated differently when multiple lenders pull your credit within the allowed FICO window. If a dealership submits your application to multiple lenders at once for the same vehicle, those pulls may count as one for scoring purposes. If the dealer ran extra pulls you never authorized, those extra inquiries can still be disputed.

Multiple mortgage inquiries made within the rate-shopping window are generally treated as one inquiry by FICO, not multiple scoring hits. That exception does not apply to credit cards, personal loans, or other revolving-credit applications.

A hard inquiry is tied to a credit application and affects your score. A soft inquiry is tied to background checks, pre-approvals, employer checks, or your own monitoring and has no scoring impact. Checking your own credit is always a soft inquiry.

Yes. You have the legal right to dispute inquiries yourself. The issue is that most online templates are too generic and do not explain the specific permissible-purpose violation well enough to force removal. That is why many DIY attempts come back verified even when the inquiry should have been challenged successfully.

Most lenders view six or more recent hard inquiries as a serious red flag, and some mortgage lenders get concerned even earlier. A stacked inquiry pattern can suppress approvals even when the rest of the credit file is workable.

If you have one or two authorized inquiries and no urgent credit goal, waiting is a reasonable choice. Their scoring impact fades with time and they fall off on their own after 24 months.

If you have several unauthorized pulls, a near-term mortgage or auto-loan goal, or an identity-theft inquiry trail, waiting is expensive. Six avoidable inquiries can mean 30 to 60 points of score damage sitting on the file while you keep paying the price in denials or worse rates. See our Arizona credit repair cost breakdown.

Every unauthorized inquiry on your report is lowering your score right now. The free consultation takes about 15 minutes. We audit every hard inquiry across Experian, Equifax, and TransUnion, tell you which ones are actually disputable, and give you a straight answer about the likely score impact.

No pressure. No obligation. We review your report first and tell you exactly what we can remove before you pay anything.

Tiene consultas no autorizadas en su reporte de credito? Ofrecemos remocion de consultas de credito en espanol para residentes de Phoenix y toda Arizona. Llame al 602-377-6626.